.svg)

Roth Conversions 101: A Framework for Understanding

You've probably heard the term "Roth conversion" thrown around. Maybe a friend mentioned it, or you read about it online. But what is it, really—and how do you know if it makes sense for you?

This isn't a deep dive into every nuance. It's a framework. If you would like a deep dive, please read this 101 article. When you finish reading, you'll understand the core logic behind Roth conversions and why they do or don't make sense in different situations.

.svg)

What is a Roth Conversion?

A Roth conversion is simply moving money from a Traditional IRA to a Roth IRA. When you do this, you pay income tax on the amount converted. In exchange, that money grows tax-free and comes out tax-free in retirement.

How Retirement Accounts Are Taxed

Understanding conversions requires understanding how these accounts work.

A Traditional IRA gives you a tax deduction when you contribute (in most cases). The money grows tax-deferred, and you pay ordinary income tax—like wages—when you take it out. Think of it this way: the IRS is your silent partner. They will be owed a percentage of every dollar in that account, and they'll collect when you withdraw.

A Roth IRA is the inverse. No deduction when you contribute, but the money grows tax-free and comes out tax-free. Every dollar is yours to spend.

A conversion is essentially settling your tax bill with the IRS early. The question: is it cheaper to settle now, or later?

What is the Benefit of a Roth Conversion? How Much Are You Really Saving?

This is another way of saying "why bother?" Let's lay out a quick example to show why people talk so much about Roth conversions.

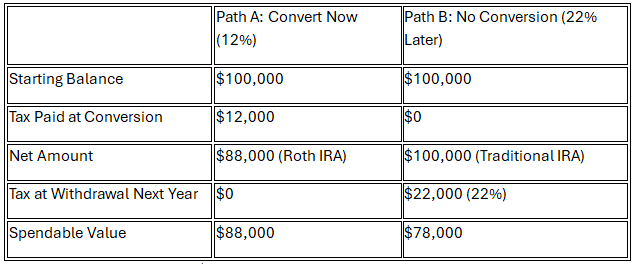

Jerry is retired and will pay no taxes this year because he has no significant sources of income. But he knows that next year—and every year moving forward—he'll have a pension and Social Security that will push him into the 22% tax bracket. If Jerry had $100,000 in Traditional IRA money, what benefit might he accrue if he converted it today?

Year 1 Example: 12% vs. 22% (No Growth)

Dollar Advantage (Convert): $10,000

By converting this year while in the 12% bracket, Jerry locks in $10,000 of permanent tax savings. At 6% growth, that $10,000 advantage becomes $32,109 after 20 years and $102,857 after 40 years—the rate differential stays the same, but time and compounding multiply the dollar benefit.

When Does a Conversion Make Sense?

A conversion is a good idea when your current tax rate is lower than your likely future rate. It's not an exact science—taxes are anything but simple—but there are times when the decision is obvious and others where it clearly doesn't make sense.

For most taxpayers, the obvious opportunities come in straightforward years: no major income swings, no large purchases, or years with significant deductions like charitable giving. The less obvious situations—income in flux, life changes on the horizon, multiple factors pulling in different directions—require running the numbers carefully.

Important Note: "Tax rate" is more complicated than the number on a bracket chart. You need to account for federal and state income taxes, Medicare premium adjustments (IRMAA), Social Security taxation, lost deductions and credits at higher income levels, and ACA health insurance subsidies if you're pre-65. All of these can be affected by the income a Roth conversion creates.

One scenario worth noting: married couples should consider their filing status trajectory. If one spouse is likely to pass away before the other, the surviving spouse becomes a single filer with significantly compressed tax brackets. Converting while both spouses are alive captures the more favorable joint brackets. This is emotionally difficult to discuss but can make a large difference for the surviving spouse.

The Bottom Line

A Roth conversion is a tax timing decision. The goal is to pay taxes when your rate is lowest.

There's no universal right answer—it depends on your income, your tax situation, your cash flow, and your time horizon. What this framework gives you is the foundation to understand why a conversion does or doesn't make sense.

Disclosures:

Important Disclosure Regarding Hypothetical Illustration

The tax example and growth projections presented above are hypothetical and are provided solely for illustrative and educational purposes. The example assumes a federal income tax rate of 12% in the year of conversion and 22% in a future year, no state income taxes, no changes to federal tax law, and a constant annual investment return of 6% compounded annually. The illustration does not account for required minimum distributions (RMDs), Medicare premium adjustments (IRMAA), taxation of Social Security benefits, phaseouts of deductions or credits, transaction costs, investment expenses, or other income-related factors that may materially affect outcomes.

The 6% annual return used in this example is hypothetical and does not represent the performance of any specific investment, portfolio, or client account. Actual investment returns will vary and may be higher or lower than the return assumed. Future tax rates and laws are subject to change and could materially impact the results shown.

This illustration does not reflect actual client experience and is not a guarantee of future results. The dollar amounts shown are based entirely on the stated assumptions and are not predictions of future performance or tax outcomes.

Roth conversions are not appropriate for all investors. Whether a conversion is beneficial depends on an individual’s specific tax circumstances, income, time horizon, investment strategy, cash flow needs, and future legislative environment. Investors should consult with their tax advisor or financial professional before implementing any conversion strategy.

This material is for informational purposes only and does not constitute investment advice, tax advice, or a recommendation to engage in any specific transaction.

.svg)

JT Stratford, LLC is an SEC-registered investment adviser. This content is for informational purposes only and does not constitute personalized investment advice. Investing involves risk, including the possible loss of principal. Additionally, while our services include tax planning, please note we do not offer specific tax services; so you will want to consult your tax preparer before implementing any tax planning strategies introduced here. Any reduction in taxes would depend on an individual’s tax situation. No information found on this website is intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor. We do not offer tax or legal advice.

.png)