.svg)

Keeping the Main Thing the Main Thing

What 2025 reminded us about investing

.svg)

If you follow sports, you’ve probably heard athletes and coaches talk about “keeping the main thing the main thing.” What is the main thing? It depends on the sport, but it usually comes down to mastering the fundamentals—the habits and disciplines required to perform at a high level over time.

Investing is no different. While there are always headlines, opinions, and short-term market movements competing for attention, long-term success has historically been driven by a few core principles. At its heart, “keeping the main thing the main thing” in investing means staying focused on what truly matters and not allowing noise or emotion to pull you off course.

As I reviewed 2025, I found myself struggling to remember much of the market noise that happened (apart from liberation day). As investors, it can be tempting to focus on year-end index returns and forget the volatility and headlines that accompanied the journey. Let’s take a step back and revisit some of 2025’s loudest moments:

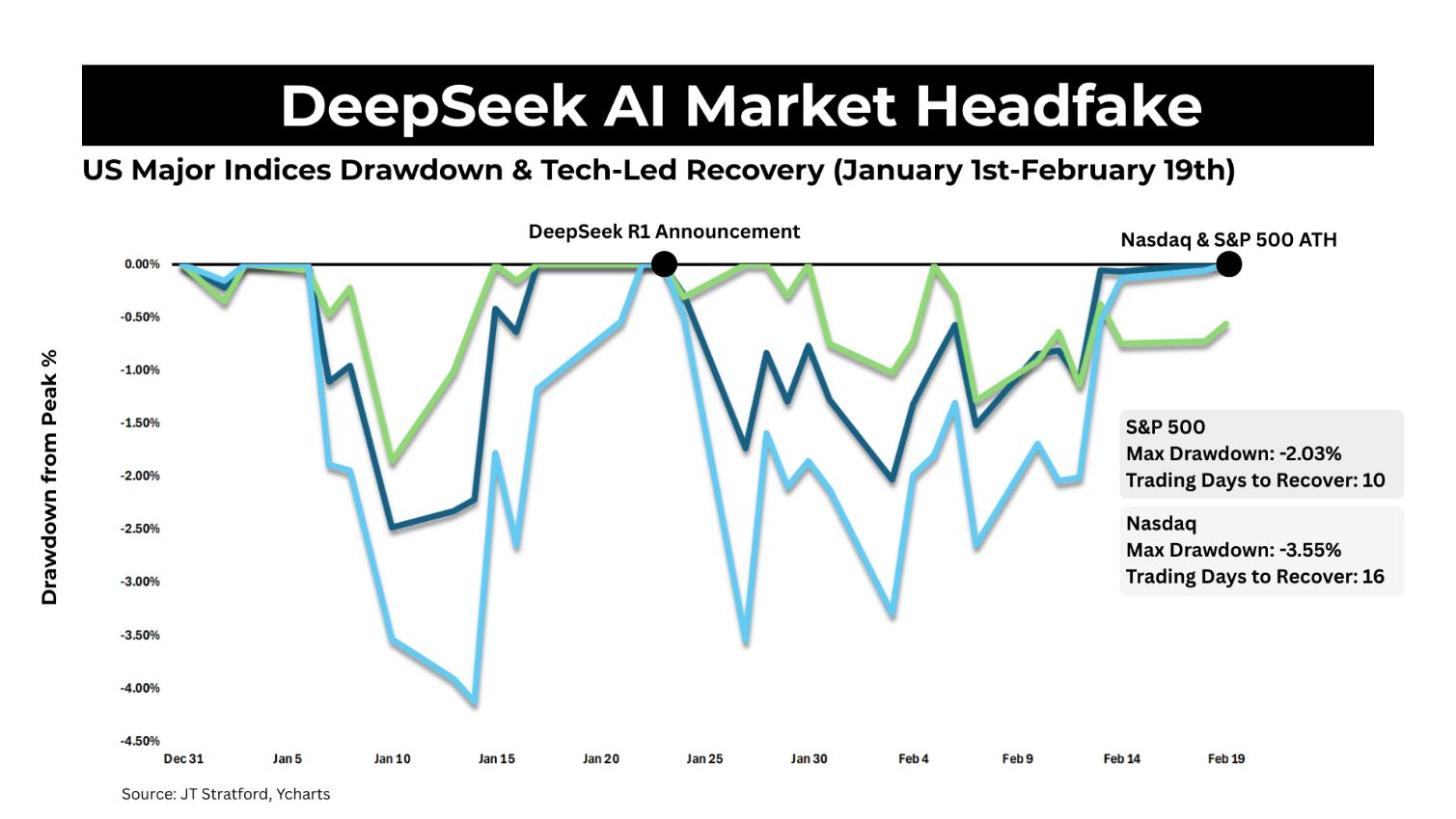

DeepSeek AI: In January 2025, investors panicked over the implications of DeepSeek’s release of its R1 reasoning model, an artificial intelligence model that performed comparably to other leading models but reportedly cost less than $6 million to develop. In response to the news, the S&P 500 fell 1.74% from its all-time highs while the Nasdaq declined 3.55%. By the middle of February, both indexes had largely recovered those losses. The initial market reaction appeared to assume that improved AI results from a foreign competitor would translate into reduced U.S. investment in artificial intelligence. That assumption missed the broader implication. The US, and specifically this administration, have never allowed foreign adversaries to hold a leg up when it comes to technology, so why would they in AI? The market reaction was just that, a reaction. We were left asking the same question, what has changed fundamentally for the long term for any of these AI companies? Our answer was largely nothing, in fact increased competition meant increased spending to win an AI arms race.

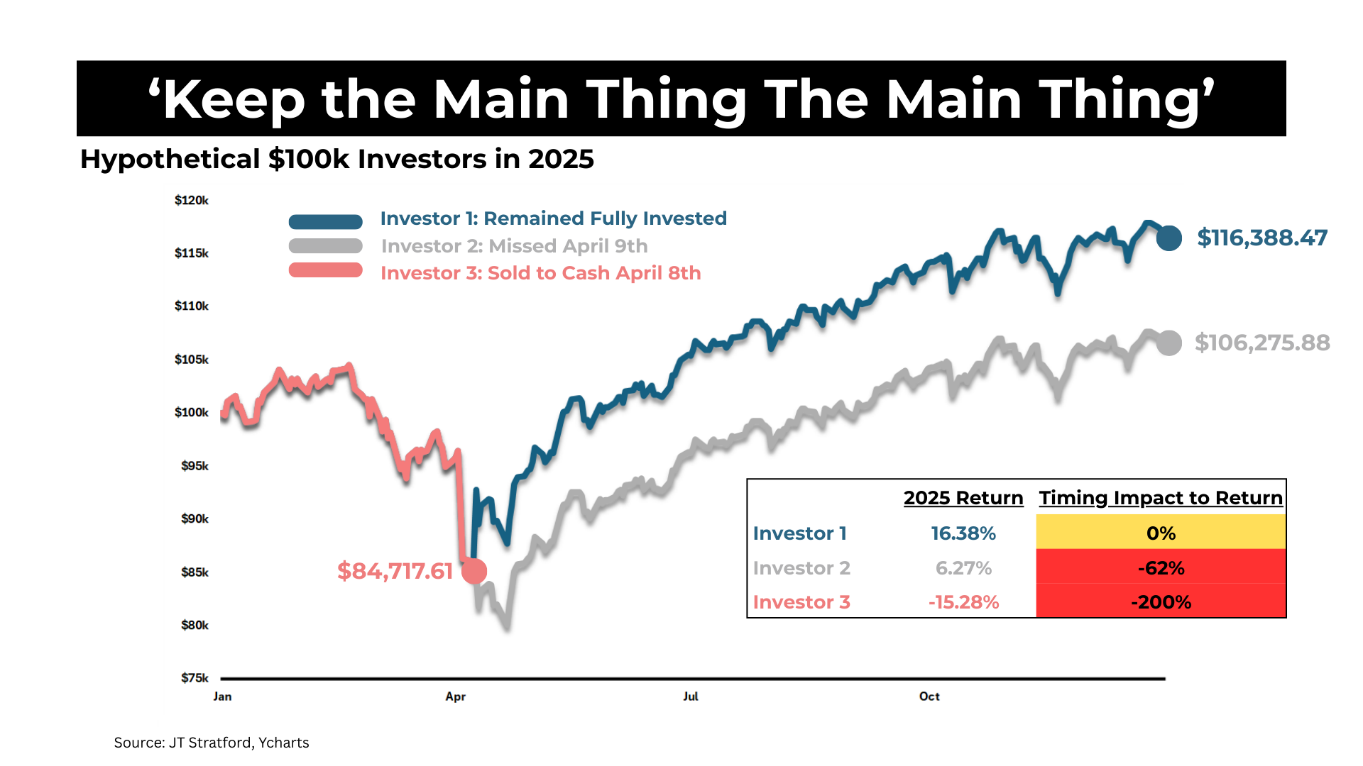

Liberation Day: In early April, the Trump Administration announced, “Liberation Day,” introducing a broad 10% tariff on most imports along with higher, country-specific reciprocal tariffs scheduled to take effect on April 9. Markets reacted swiftly, with equities falling sharply and the Nasdaq officially entering bear market territory. The sudden drop erased $3.1 trillion in market value in a single session, spooking investors. Yet on April 9th, a 90-day pause on the tariffs sparked a sharp rebound. This rapid turnaround showed just how quickly expectations can shift. More importantly, it underscored the risks of making investment decisions based on short-term headlines or policy noise. Liberation day showed the value of focusing on long-term fundamentals, even amid extreme market volatility.

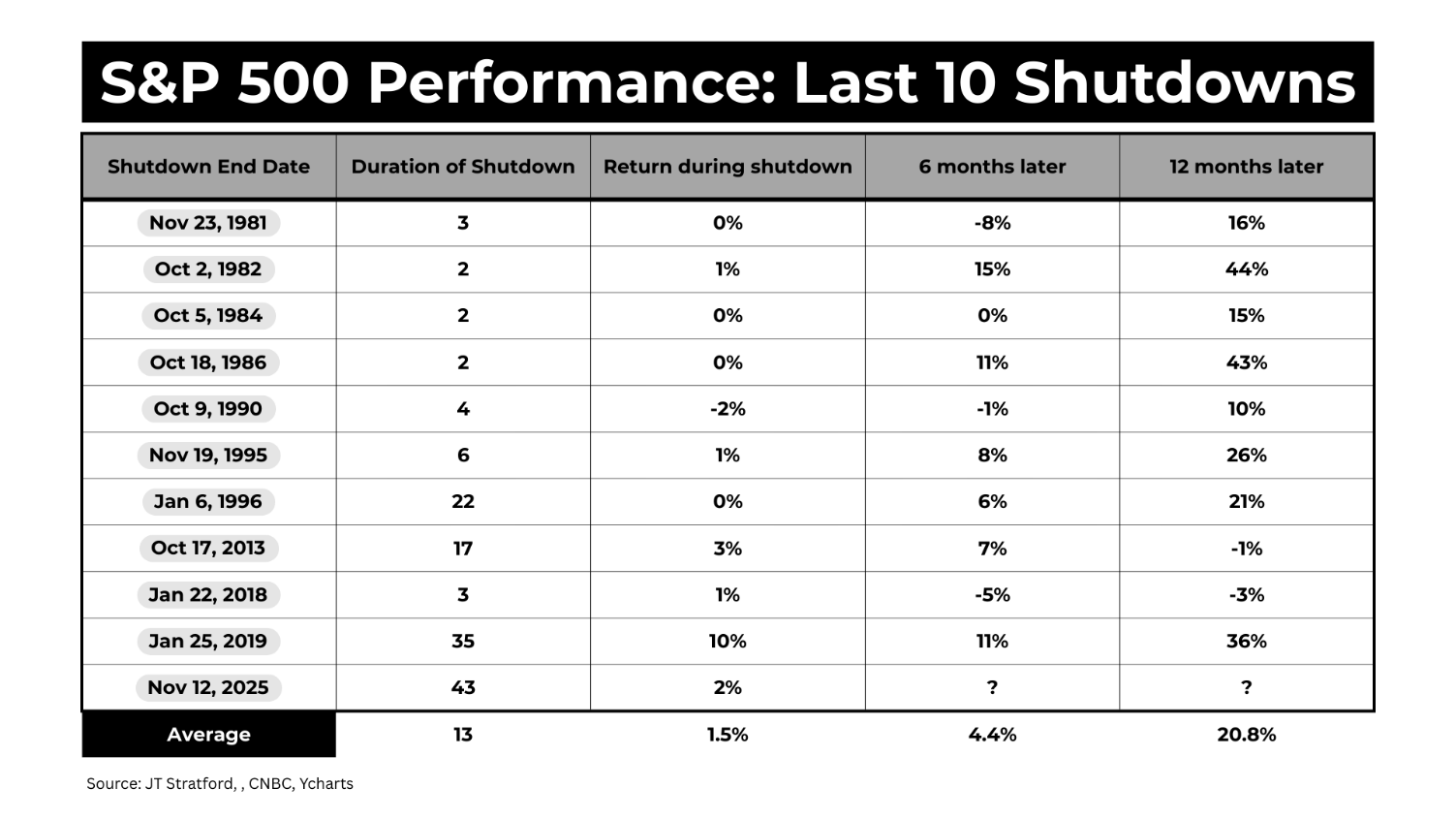

Government Shutdown: Congress was unable to reach agreement on appropriations or a stopgap measure before the September 30 deadline, triggering a government shutdown which began on October 1st. The shutdown stretched for 43 days, becoming the longest in US history before a bipartisan funding measure was approved in mid-November. Markets remained relatively agnostic to the political impasse on Capitol Hill, despite several widely cited concerns, including missed federal paychecks, operational uncertainty within the aviation system, and delays in the release of key economic data.

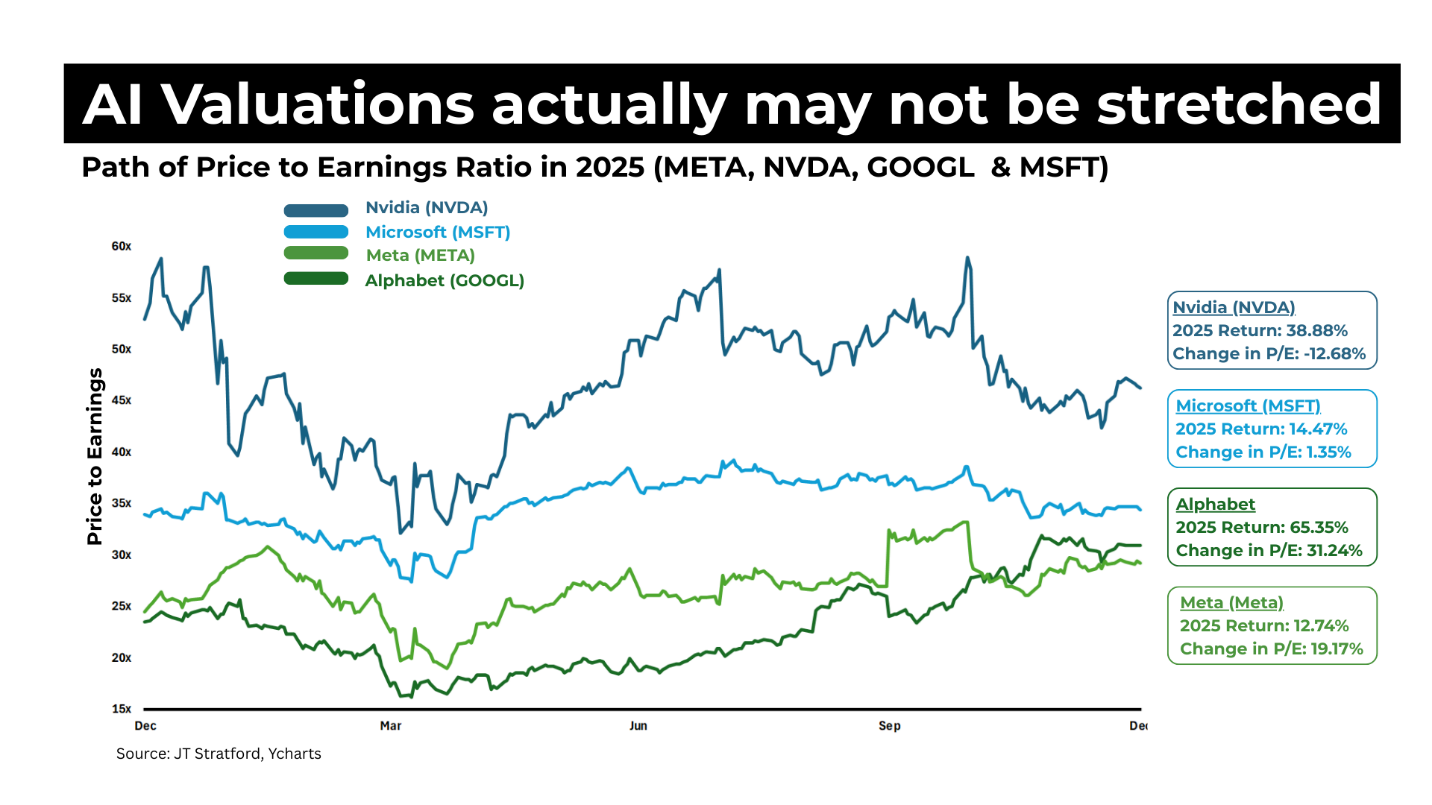

AI Bubble Fears: Scrutiny around a potential AI stock bubble intensified in November. Concerns over circular funding dynamics, massive capital expenditure requirements, and “stretched” valuations pushed major equity indices off their highs once again, with markets reaching a recent low on November 19—the same day Nvidia reported earnings. During the earnings call, Nvidia CEO Jensen Huang directly addressed the growing bubble narrative. “There’s been a lot of talk about an AI bubble,” Huang said. “From our vantage point, we see something very different.” He went on to frame AI not as a speculative cycle, but as a fundamental shift toward accelerated computing. That raises an important question: what defines a stock market bubble? Typically, bubbles share a combination of characteristics—rapid price appreciation, valuations well above historical norms, compelling narratives, and a fear of missing out that drives behavior more than fundamentals. Much of the AI “bubble” discussion has centered on valuation. The chart below shows four of the largest AI-related companies and the path of their price-to-earnings ratios over the year. Despite returning nearly 40% in 2025, Nvidia’s price-to-earnings ratio declined by 12.68%. Given that valuation is simply price divided by earnings, this means earnings growth more than offset the increase in share price. In other words, while prices rose, fundamentals improved even faster—an outcome that runs counter to how bubbles typically form. That doesn’t mean risks don’t exist, but it does suggest that labeling the entire AI trade as a “bubble” may oversimplify what has so far looked less like speculative excess and more like rapid fundamental adoption catching up with historic demand.

Despite the noise and volatility, U.S. markets delivered strong gains in 2025, with the Nasdaq up 21%, the S&P 500 up 18%, and the Dow up 15%. These results reinforce a key lesson: short-term headlines and market swings may grab attention, but long-term fundamentals drive returns. Staying disciplined, “Keeping the Main Thing the Main Thing”, and maintaining a long-term perspective allowed investors to navigate the year successfully.

Disclosure:

This material is provided for informational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future results. Index returns are shown for illustrative purposes only, do not represent the performance of any client account, and do not reflect the deduction of advisory fees or expenses. Investors cannot invest directly in an index. All index performance figures cited refer to the calendar year ended December 31, 2025.

.svg)

JT Stratford, LLC is an SEC-registered investment adviser. This content is for informational purposes only and does not constitute personalized investment advice. Investing involves risk, including the possible loss of principal. Additionally, while our services include tax planning, please note we do not offer specific tax services; so you will want to consult your tax preparer before implementing any tax planning strategies introduced here. Any reduction in taxes would depend on an individual’s tax situation. No information found on this website is intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor. We do not offer tax or legal advice.

.png)