.svg)

Stablecoins

Stablecoins are one of the fastest growing innovations in the digital finance space, designed to combine the stability of fiat currency with the efficiency of blockchain technology. Essentially functioning as a digital dollar, offering faster settlement, lower transaction costs and broader dollar access to underbanked individuals domestically and abroad.

.svg)

At their core, stablecoins are digital assets created to maintain a constant value relative to a reference currency, most often the US dollar. They can be thought of as digital cash: holding ten dollar-pegged stablecoins is functionally equivalent to holding ten dollars in purchasing power. They are issued by private entities and circulate on public blockchains such at Bitcoin.

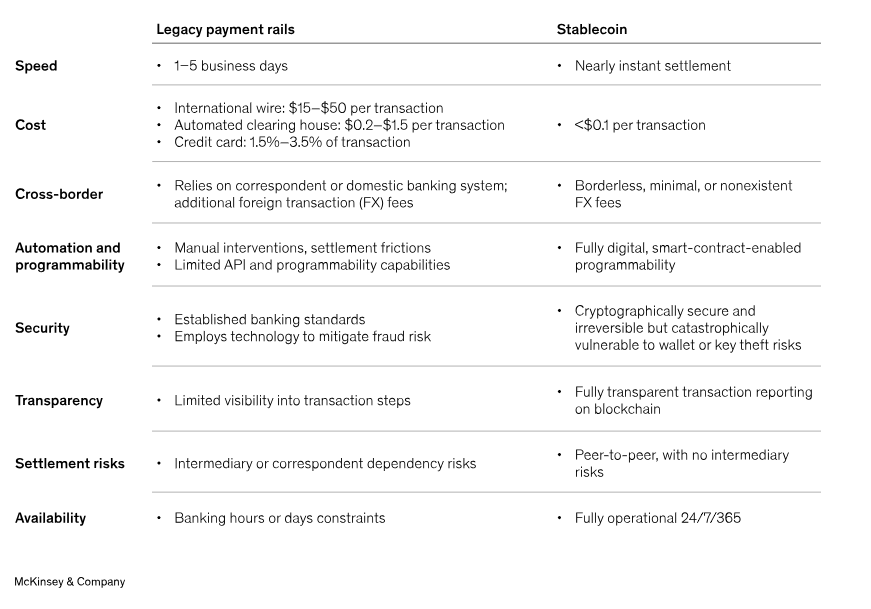

The rationale for stablecoins stems from the limitations of both traditional payments and existing cryptocurrencies. Assets like Bitcoin and Ethereum are innovative but volatile, which undermines their utility as mediums of exchange. Stablecoins, by contrast, are designed to maintain consistency in value, bridging the gap between digital assets and traditional money. Compared with legacy payment systems, they offer several advantages. Settlement that typically takes one to three business days-or longer for cross border transactions- can occur in seconds. Costs are substantially lower, as the multiple intermediaries in card and bank transactions are removed. Transparency improves because transactions on a blockchain are verifiable in real time, while traditional infrastructure may be routed through multiple financial institutions before reaching its intended recipient, which makes it difficult to determine when payments will be received. And unlike banking systems that close outside of business hours, stablecoins are available 24/7/365. So that friend that lives in London can send you $1,000 via stablecoin at 11:07pm on a Saturday in under a minute for minimal cost-no banking hours, no intermediaries. Perhaps most importantly, stablecoins extend access to billions of people who remain outside of the traditional financial system, providing inclusion into financial markets through nothing more than a digital wallet. 1

While current usage is largely concentrated in crypto-to-fiat exchanges, adoption is expected to broaden into areas such as merchant payments, cross-border remittances and institutional settlement. Still this opportunity comes with risks. Like banks, issuers must manage liquidity and solvency. But there are also unique considerations, most notably the possibility of “depegging.” It is important to differentiate that a stablecoin isn’t a dollar; its an IOU for $1. Because its an IOU, the price can drift from $1. Since stablecoins are intended to maintain a one-to-one value with the US dollar, a deviation from the parity- say, requiring two tokens to equal one dollar-would undermine their fundamental purpose. Issuers mitigate this risk by maintaining reserves of cash and short-term treasuries, a structure reminiscent of the gold standard that once anchored the dollar.

Regulatory clarity is another key variable. For more than a decade, the digital asset space has operated under fragmented oversight, with overlapping jurisdictions and limited guidance. This landscape began to shift meaningfully this summer. The GENIUS act, now law, establishes a framework for US payment stablecoins, including reserve requirements, oversight and compliance obligations2. It overwhelmingly passed with rare bipartisan support in both chambers of Congress. Additional proposals- the CLARITY act, which seeks to define the roles of the SEC and CFTC and the Anti-CBDC Surveillance State Act, which would prohibit a Federal Reserve issued digital currency- underscore how central stablecoins have become to policy debate.

Despite their rapid adoption, stablecoins do not currently pose a threat to the US dollar’s global role. In fact, the Department of Treasury provided a summary in April that indicated stablecoins could increase the US Dollar’s global presence, because the overwhelming majority are pegged to and backed by the dollar3. Stablecoins essentially act as digital wrappers for dollars, expanding their reach into new markets and digital ecosystems, particularly in regions where banking access is limited or local currencies are unstable. This dynamic extends beyond currency dominance to U.S. debt markets as well. The reserves backing fiat-pegged stablecoins are predominantly held in cash and short-term U.S. Treasuries, creating additional demand for U.S. government securities. As stablecoin adoption grows, this demand could serve as a stabilizing force for Treasury markets, deepening liquidity and reinforcing the central role of U.S. assets in the global financial system.

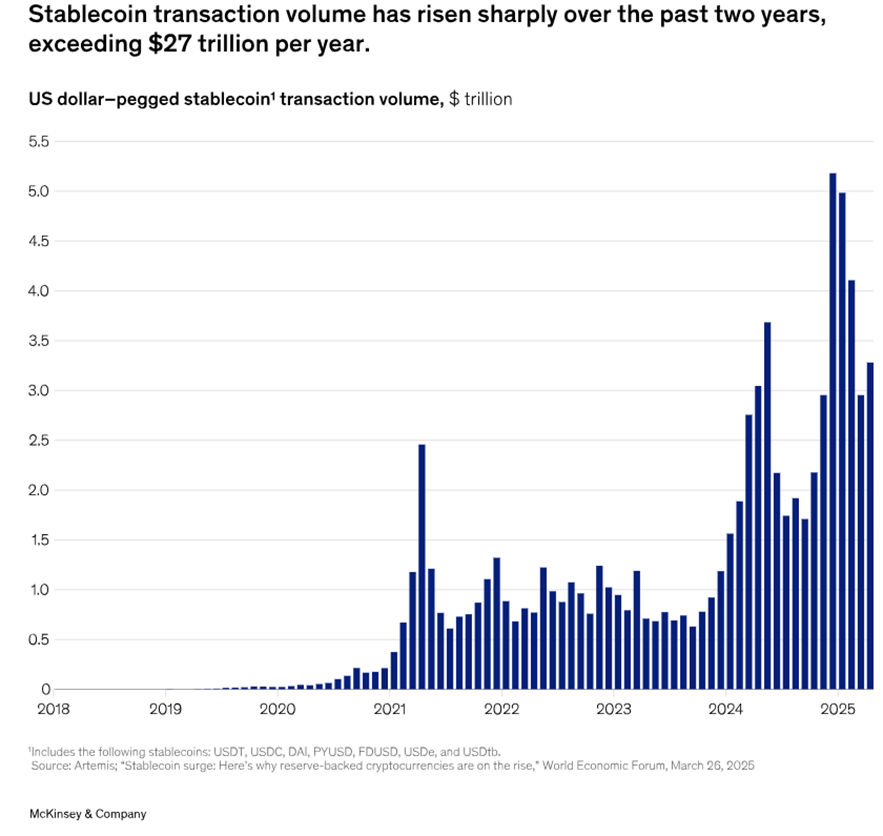

Stablecoins, then, are no longer a niche innovation. They represent an evolving bridge between traditional finance and blockchain technology, with the potential to modernize payments at scale. For investors and institutions, the question is not whether stablecoins will matter, but how quickly adoption will grow and under what regulatory frameworks. With daily volumes poised to expand from $30 billion today (Visa’s daily transaction volume is approximately $38.9 billion daily) to potentially $2 trillion within the next few years, stablecoins are positioned to play a central role in the future of global finance.

1 https://www.mckinsey.com/industries/financial-services/our-insights/the-stable-door-opens-how-tokenized-cash-enables-next-gen-payments

2 https://www.congress.gov/bill/119th-congress/senate-bill/1582/text

3 https://home.treasury.gov/system/files/221/TBACCharge2Q22025.pdf

.svg)

JT Stratford, LLC is an SEC-registered investment adviser. This content is for informational purposes only and does not constitute personalized investment advice. Investing involves risk, including the possible loss of principal. Additionally, while our services include tax planning, please note we do not offer specific tax services; so you will want to consult your tax preparer before implementing any tax planning strategies introduced here. Any reduction in taxes would depend on an individual’s tax situation. No information found on this website is intended to be a substitute for specific individualized tax advice. We suggest that you discuss your specific tax issues with a qualified tax advisor. We do not offer tax or legal advice.

.png)